Will this plan work in conjunction with an individual health insurance plan that I have already purchased?

Yes. Absolutely.

Does the proposed plan apply to or is it useful to those who are NRI—permanently based abroad but spending sizable time in India?

Yes, since this policy permits claims that arise in India and for hospitalizations within the borders of India.

Is a base policy in my name a requisite for this plan? If I am covered up to ₹3 Lacs by my spouse's policy, can I go ahead and enrol in this Super Top-up plan without having a base policy in my name?

A base policy is not a prerequisite. Yes, you can enrol with the minimum deductible option of ₹3 Lacs.

I have a base policy from my employer where there is no waiting period. If I take the Super Top-up this year but leave my job next year, what happens to the waiting period when I renew the Super Top-up plan?

The Super Top-up policy functions independently of the employer-provided base policy. It will get triggered once you cross the chosen deductible amount.

Why are aspects like maternity not part of it?

Maternity claims rarely go beyond ₹3 Lacs, which are usually covered under the base policy. Additionally, the event is limited to a specific section of the population and most corporate policies already cover it.

Will the Super Top-up work even if there is no base plan? i.e., can the ₹5 Lakh deductible be covered through self-insurance?

Yes. This will also work if you are paying the deductible out of pocket.

If we choose base deductible as ₹10 Lacs, and have a base policy of ₹3 Lacs with one insurer, and a ₹10 Lacs Super Top-up with another provider (with ₹3 Lacs deductible), will the Super Top-up work beyond ₹10 Lacs? How will cashless be settled?

If you have chosen a Super Top-up plan with a ₹10 Lacs deductible, you will need to produce payment receipts up to ₹10 Lacs (paid by you or any policy). Beyond that, cashless settlement will occur in the network hospital up to the insured sum.

Is there any limit on the claim amount for each person in the policy?

No individual claim limit—alumni can claim up to the total sum insured. The policy is triggered after crossing the deductible amount.

What if your base plan is in the US but covers medical expenses out of the US, including India. Will all expenses above deductible be covered by the Super Top-up policy?

Yes, for hospitalizations in India. However, the deductible must also be spent in India for the Super Top-up policy to activate.

If I am diagnosed outside of India, can I avail this policy if I seek treatment within India?

Yes.

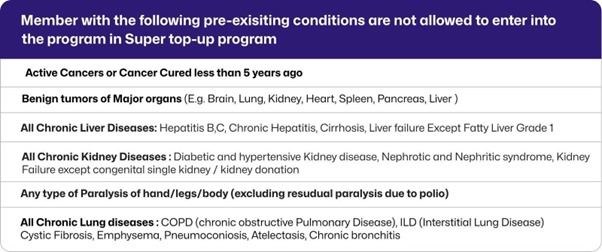

Does the basic scheme not provide coverage? Is it only available with a certain deductible (seems to start from ₹3 Lakh or ₹5 Lakh)? Will the claim settlement and enrolment process be online?

This is a Super Top-up insurance plan, which requires selection of a deductible. The entire enrolment and claims process is online through the JGEC Alumni Portal and the insurer’s digital portal.

Can policies already in force be continued concurrently?

Yes. The Super Top-up functions independently. To trigger it, alumni must submit proof of claim payment (claim settlement letter or receipt). Once the deductible threshold is crossed, the Super Top-up coverage kicks in.

Since it is a top-up insurance and hospitals will bill only once, how will the remaining amount be settled with the base insurer?

Once the deductible amount is met—either through another policy or out-of-pocket—the Super Top-up is triggered. All subsequent eligible claims are covered under this policy.

Is there any coverage for outpatient procedures or home treatments like nurse visits, where hospitalization isn't involved?

No. This is an IPD-only (In-Patient Department) program. However, home hospitalization is covered.

Does Zopper only offer Super Top-up coverage, or do they also provide base policy products?

Currently, Zopper is offering only the Super Top-up plan. The base policy may be considered in the second year based on alumni demand.